about me¶

- applied econometrics, computer science (Master)

- economic theory (PhD)

- software for statistics and economtrics

- user-developer with various packages and with GAUSS, Matlab, Python

- scipy.stats

- statsmodels

- "self-taught statistician"

about statsmodels¶

- precursor: scipy.stats.models

- 7 years of development

- started with GSOC Skipper Seabold

- slow and steady growth since then

- GSOC Chad Fulton statespace models

- open source, BSD licensed

- ~ 130,000 LOC of Python (including some Cython)

Brief Overview - Time Series Analysis in Statsmodels¶

- Data Handling through Pandas

- statistics

- acf, pacf

- filters, seasonal decomposition

- hypothesis tests: unit root, Granger causality

- ARMA, ARIMAX

- VAR (vector autoregressive models)

- new statespace models

- SARIMAX

- ...

- postestimation: predict, impulse response, hypothesis testing

two GSOC projects in 2016 for TSA

%matplotlib inline

import datetime

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from dateutil.relativedelta import relativedelta

import seaborn as sns

import statsmodels.api as sm

import statsmodels.formula.api as smf

from statsmodels.tsa.stattools import acf

from statsmodels.tsa.stattools import pacf

from statsmodels.tsa.seasonal import seasonal_decompose

#plt.interactive(False) # otherwise interactive(False)

El Nino temperature data¶

from statsmodels.datasets.elnino import load_pandas

datadf = load_pandas()

datadf.data

temperature = np.asarray(datadf.data.iloc[:, 1:]).ravel()

nobs = len(temperature)

index = pd.date_range("1950-01-01", periods=nobs, freq='MS')

months = np.tile(np.arange(12), nobs // 12)

df_el = pd.DataFrame({'temperature': temperature, 'month': months}, index=index)

df_el.tail()

ax = df_el['temperature'].plot()

ax.figure.set_size_inches(12, 8)

ax.set_title('Temperature', fontsize=18)

ax = df_el['temperature'].iloc[-12*5:].plot(style='-o')

ax.figure.set_size_inches(12, 8)

_ = ax.set_title('Temperature', fontsize=18)

res_ols = sm.formula.ols('temperature ~ C(month)', df_el.iloc[:-3*12]).fit()

predicted = res_ols.predict(df_el.iloc[-3*12:])

fitted = res_ols.fittedvalues.loc['2005-12-01':] # 5 years

ax = df_el['temperature'].iloc[-12*5:].plot(style='-o')

ax.figure.set_size_inches(12, 6)

fitted.plot(lw=2, color='r')

predicted.plot(lw=2, color='r')

ax.vlines(predicted.index[0], lw=4, alpha=0.25, *ax.get_ylim())

_ = ax.set_title('Constant Seasonal Pattern - fitted and predicted', fontsize=18)

ax = res_ols.resid.iloc[-5*12:].plot(style='-o',figsize=(12,8))

_ = ax.set_title('Residuals insample', fontsize=18)

_ = cfplot(res_ols.resid, lags=36)

import patsy

y, x = patsy.dmatrices('temperature ~ C(month)', df_el, return_type='dataframe')

res_arma = sm.tsa.ARMA(y, order=(2, 1), exog=x.iloc[:, 1:]).fit()

print(res_arma.summary())

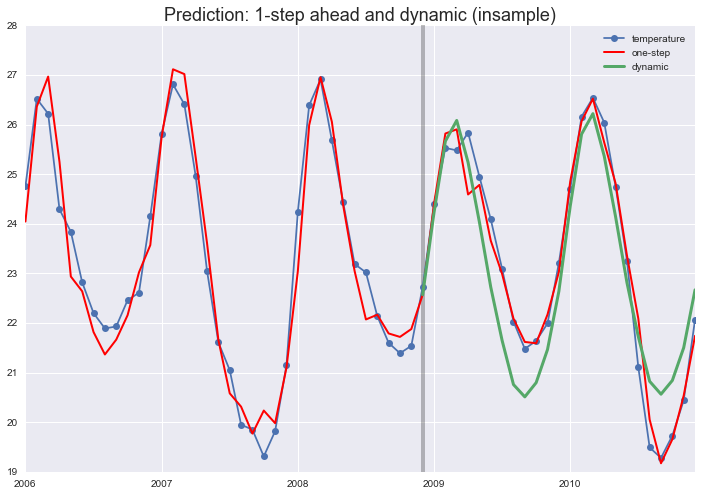

pred_dynamic = res_arma.predict(start='2008-12-01', end='2010-12-01', exog=res_arma.model.exog[-3*12:, 1:], dynamic=True)

fitted = res_arma.fittedvalues

Short term and long term forecasts¶

Summary ARMAX¶

y = X b + e, e ~ ARMA(p, q)¶

use explanatory variables X to model stable, systematic part¶

- seasonal patterns: dummies, splines, fourier polynomials

- trend: linear, polynomial, or piecewise

- other effects: dummies for special events, outliers

- explanatory variables: related series that help in prediction, (need forecasts for those, or use lagged values)

use ARMA to improve short term forecasting¶

- e = y - X b

- use the additional information that is left after systematic part has been removed

- assumes what is left over is stationary

Stationarity¶

A time series is stationary if the distribution of the observations does not depend on time.¶

Often only mean, variance and autocovariance stationarity is relevant

no persistence: shocks or disturbances have not long term effect

mean reversion: the long term forecast moves to the mean of the series

Random Walk y(t) = y(t-1) + e(t)¶

The best forecast at time t $\hat{y}(t+1) = y(t)$ and $\hat{y}(t+h) = y(t)$

Tomorrow is like today.

seasonal y(t) = y(t - s) + e(t)

Tomorrow is like the same day last week (month, year)

full persistence: every shock stays forever¶

y(t) is integrated, the differenced series is stationary

substituting back in

$y(t) = y(0) + \sum_{i=1}^{t} e(t-i)$

SARIMAX without X¶

SARIMAX(endog, exog=None, order=(1, 0, 0), seasonal_order=(0, 0, 0, 0), trend=None, ...)¶

endog is endogenous, dependent variable (statsmodels econometrics history)

exog are eXogenous, independent, explanatory variables

order (p, d, q) is regular ARIMA

seasonal_order (P, D, Q, s) is seasonal ARIMA with season length s

example: SARIMA((1, 0, 0), (1, 0, 0, 12) only AR terms

$(1 - a_1 \hspace{2mm} L) (1 - A_1 \hspace{2mm} L^{12}) y_t = y_t - a_1 \hspace{2mm} y_{t-1} - A_1 \hspace{2mm} y_{t-12} + a_1 \hspace{2mm} A_1 \hspace{2mm} y_{t-13}$¶

$y_t = a_1 \hspace{2mm} y_{t-1} + A_1 \hspace{2mm} y_{t-12} - a_1 \hspace{2mm} A_1 \hspace{2mm} y_{t-13} \hspace{2mm} + ...$¶

Model Selection and Automatic Forecasting¶

Hyndman has several supporting functions in R, auto.arima

statsmodels doesn't have much ready made and automatic

Amount of Differencing¶

(standard maximum likelihood methods do not apply)

commonly based on unit root or stationarity tests

Lag lengths, p, q, P, Q¶

loop over set of lag lengths and choose the model

minimize AIC, BIC, or maximize out-of-sample forecast performance.

Outliers, ...¶

dummies for outlier observation, trend breaks, ...

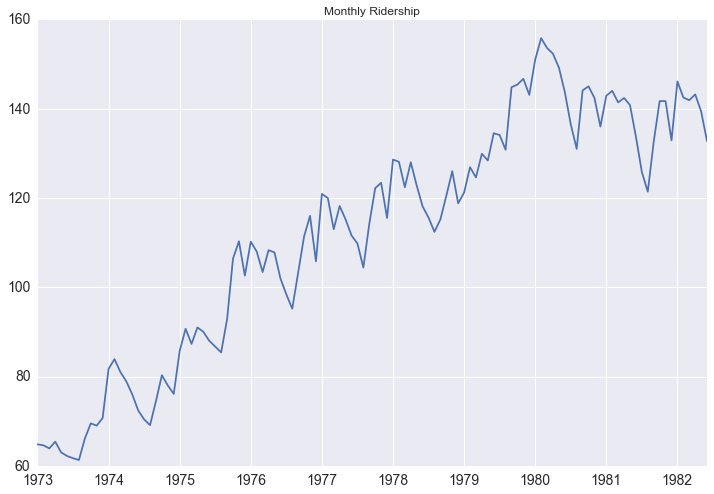

Example: Forecasting Bus Riders¶

see blog post and notebook for details

http://www.seanabu.com/2016/03/22/time-series-seasonal-ARIMA-model-in-python/

seas = seasonal_decompose(df['riders'])

fig = seas.plot()

fig.set_size_inches(12,8)

mod = sm.tsa.statespace.SARIMAX(df.riders, order=(0,1,0), seasonal_order=(1,1,1,12), trend='n')

results = mod.fit()

results.summary()

df['forecastd'] = results.predict(start=102, end=114, dynamic=True)

df['forecastnd'] = results.predict(start=102, end=114, dynamic=False)

df[['riders', 'forecastd', 'forecastnd']].loc['1979-01-01':].plot(figsize=(12, 8), color='brk', lw=3, alpha=0.5)

plt.savefig('images/ts_df_predict.png', bbox_inches='tight')

SARIMAX and transformation¶

back to the initial plot

df_air = pd.read_csv('AirPassengers.csv', index_col=0)

di = pd.date_range("1949-01-01", periods=144, freq='MS')

df_air.set_index(di, inplace=True)

del df_air['time']

df_air.tail()

df_air.plot(figsize=(12,6))

plt.savefig('air_passenger.png', bbox_inches='tight')

air_log = np.log(df_air['AirPassengers'])

air_log.plot(figsize=(12,6))

Rolling Standard Deviation - orginal versus log transformed¶

fig, (ax1, ax2) = plt.subplots(2, 1, sharex=True, figsize=(12,6))

_ = df_air['AirPassengers'].rolling(12).std().plot(ax=ax1)

_ = air_log.rolling(12).std().plot(ax=ax2)

Rolling Standard Deviation - Box-Cox transformed¶

from scipy import special

ax = special.boxcox(df_air['AirPassengers'], -0.2).rolling(window=12).std().plot(figsize=(12,6))

def box_cox_rolling_coeffvar(box_cox_param, endog, freq):

"""helper to find Box-Cox transformation with constant standard deviation

returns RLM results instance

"""

roll_air = special.boxcox(endog, box_cox_param).rolling(window=freq)

y = roll_air.std()

m = roll_air.mean()

x = sm.add_constant(m)

res_rlm = sm.RLM(y, x, missing='drop').fit()

return res_rlm

endog = df_air['AirPassengers']

freq = 12

tt = [(lam, box_cox_rolling_coeffvar(lam, endog, freq).pvalues[1]) for lam in np.linspace(-1, 1, 21)]

tt = np.asarray(tt)

print(tt[tt[:,1].argmax()])

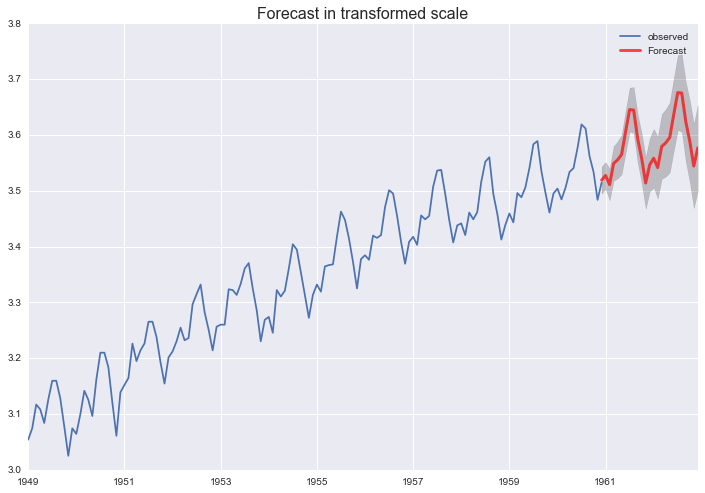

SARIMAX((1, 1, 1), (0, 1, 1, 12)) of transformed series¶

air_t = special.boxcox(df_air['AirPassengers'], -0.2)

res_s = sm.tsa.SARIMAX(air_t, order=(1, 1, 1), seasonal_order=(0, 1, 1, 12)).fit()

res_s.summary().tables[1]

max_ar, max_ma = 3, 3

aic_full = pd.DataFrame(np.zeros((max_ar, max_ma), dtype=float))

# Iterate over all ARMA(p,q) models with p,q in [0,1, 2]

for p in range(max_ar):

for q in range(max_ma):

if p == 0 and q == 0:

continue

# Estimate the model with no missing datapoints

mod = sm.tsa.statespace.SARIMAX(air_t, order=(p,1,q), seasonal_order=(0, 1, 1, 12), trend='c', enforce_invertibility=False)

try:

res = mod.fit()

aic_full.iloc[p,q] = res.aic

except:

aic_full.iloc[p,q] = np.nan

print('min at ', np.asarray(aic_full).argmin())

aic_full

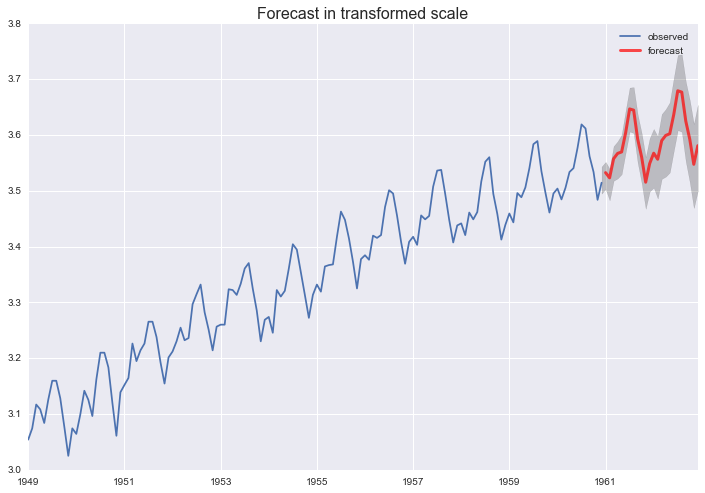

pred = res_s.get_prediction(start='1960-12-01', end='1962-12-01')

pred_ci = pred.conf_int()

Transform forecast to original scale¶

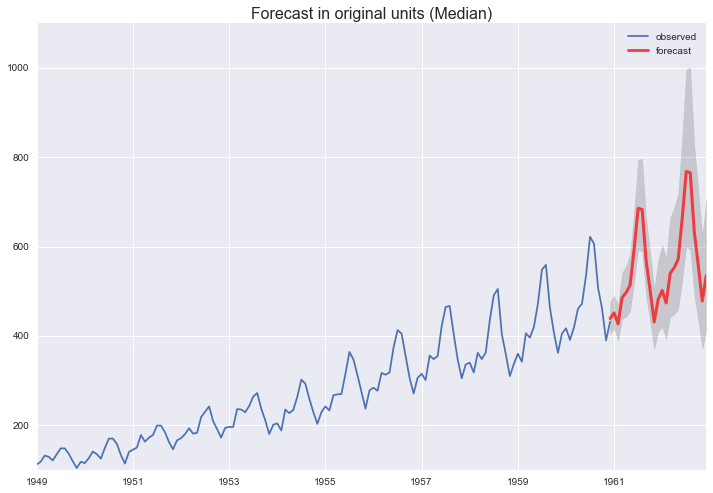

pred_ci_orig = special.inv_boxcox(pred.conf_int(), -0.2)

forecast = special.inv_boxcox(pred.predicted_mean, -0.2)

ax = df_air['AirPassengers'].plot(label='observed')

ax.figure.set_size_inches(12, 8)

forecast.plot(ax=ax, label='forecast', lw=3, alpha=.7, color='r')

ax.fill_between(pred_ci_orig.index,

pred_ci_orig.iloc[:, 0],

pred_ci_orig.iloc[:, 1], color='k', alpha=.15)

ax.set_title('Forecast in original units (Median)', fontsize=16)

plt.legend()

plt.savefig('images/airpassenger_forecast.png', bbox_inches='tight')

mod_ucarima = sm.tsa.UnobservedComponents(air_t, 'lltrend', seasonal=12, autoregressive=4)

res_ucarima = mod_ucarima.fit(method='powell', disp=0)

print(res_ucarima.summary())

fig_uc = res_ucarima.plot_components()

fig_uc.set_size_inches(12, 8)

pred_uc = res_ucarima.get_forecast(steps=24)

pred_ci = pred.conf_int()

#pred_uc.predicted_mean

References¶

documentation¶

http://www.statsmodels.org/dev/tsa.html

http://www.statsmodels.org/dev/statespace.html

http://www.statsmodels.org/dev/examples/index.html

blog posts¶

http://tomaugspurger.github.io/modern-7-timeseries.html Pandas usage

http://www.seanabu.com/2016/03/22/time-series-seasonal-ARIMA-model-in-python/

http://www.analyticsvidhya.com/blog/2016/02/time-series-forecasting-codes-python/

I will clean up notebook during weekend